When Are Tax Returns Due? UK Deadlines 2025/26

What Is a Tax Return?

When Are Tax Returns Due? This is one of the most common questions asked by UK business owners, self-employed individuals, landlords, and company directors. Understanding tax return deadlines is essential because missing a filing date can result in HMRC penalties, interest charges, and unnecessary stress.A tax return is a formal submission to HMRC that reports income, gains, expenses, reliefs, and tax liabilities for a specific tax period. HMRC uses this information to calculate how much tax is due or whether a refund is owed.Tax return deadlines are critical dates that UK small business owners must meet annually. Missing a deadline can trigger costly HMRC penalties and interest charges automatically. Whether you are self-employed, run a limited company, or manage rental income, understanding the deadlines is essential. This guide covers all UK tax return due dates, extensions, and penalty implications for 2025/26.

Key Takeaways

- Self Assessment returns for self-employed and landlords must be filed by 31 January following the tax year end, or 31 October for paper filing.

- Corporation tax returns for limited companies have a nine-month filing deadline from the accounting period end date.

- HMRC penalties begin at £100 for returns filed between one and three months late, escalating to up to 5% of unpaid tax if filed over 12 months late.

- Extensions are available in limited circumstances: request by telephone before the deadline or claim reasonable excuse if circumstances change after filing.

- Making Tax Digital mandatory filing applies to VAT, Self Assessment income tax, and corporation tax, with specific online submission requirements and deadlines.

UK tax return deadlines vary by business type. Self-employed and landlords filing online have until 31 January following the tax year end. Limited companies must file corporation tax returns within nine months of their accounting period end. Paper Self Assessment returns must be filed by 31 October.

In Short

- Online Self Assessment: 31 January 2027 (for 2025/26 tax year)

- Paper Self Assessment: 31 October 2026

- Corporation tax: Nine months from accounting period end

- VAT returns: 7 days from month end

Need help with your tax return? Speak to our ICAEW-qualified team today.

Tax Return Deadlines at a Glance

|

Return Type |

Filing Deadline |

Payment Deadline |

|

Self Assessment (Online) |

31 January 2027 |

31 January 2027 |

|

Self Assessment (Paper) |

31 October 2026 |

31 January 2027 |

|

Partnership Return (Online) |

31 January 2027 |

N/A |

|

Partnership Return (Paper) |

31 October 2026 |

N/A |

|

Corporation Tax Return (CT600) |

12 months after accounting period end |

Corporation Tax due 9 months and 1 day after period end |

|

VAT Return |

Usually 1 month and 7 days after VAT period end |

Same deadline as VAT payment |

What Are the Key UK Tax Return Deadlines You Must Know?

UK tax return deadlines vary significantly depending on your business structure and how you file. The tax year runs from 6 April to 5 April annually. For the 2025/26 tax year (6 April 2025 to 5 April 2026), different taxpayer categories face different submission deadlines. Self-employed traders and landlords have until 31 January 2027 to file online, whilst limited companies must file within nine months of their accounting period end.

Missing a deadline triggers automatic HMRC penalties, even if you have no additional tax to pay. Understanding which deadline applies to your business is the first step to compliance. HMRC enforces these dates strictly; there are no automatic extensions.

The annual tax year structure in the UK

The UK tax year always ends on 5 April. This is not a filing deadline—it is simply when one tax year closes and the next begins. The filing deadlines come after the tax year ends. For 2025/26, the tax year ends 5 April 2026, but your return is due 31 January 2027 (online) or 31 October 2026 (paper).

Why deadlines matter for small businesses

Missed deadlines cost money beyond taxes owed. HMRC applies automatic penalties without requiring a formal notice. Late filing penalties, late payment interest, and potential enquiry costs add up quickly. Staying ahead of deadlines protects your cash flow and prevents stress.

The three main taxpayer categories

- Self-employed and landlords: File Self Assessment returns by 31 January online (or 31 October for paper).

- Limited company directors: File corporation tax returns within nine months of accounting period end.

- Partnership members: File partnership returns by 31 January; individual partners then file personal Self Assessment returns.

Source: HMRC Self Assessment: Due dates and deadlines

[ Self Assessment tax return service for self-employed and landlords]

When Is the Self Assessment Deadline for Self-Employed and Landlords?

Self-employed traders and landlords filing online must submit their Self Assessment returns by 31 January following the tax year end. For the 2025/26 tax year, this is 31 January 2027. Paper returns must be submitted by 31 October 2026—three months earlier. Filing online gives you significantly more time and is strongly recommended by HMRC as it reduces filing errors and penalties.

Paper return deadline vs. online deadline

Paper Self Assessment returns must reach HMRC by 31 October 2026 for the 2025/26 tax year. Online returns have until 31 January 2027. The extra three months for online filing is a significant advantage, especially if you need time to gather records or work with an accountant. HMRC no longer accepts paper returns from most taxpayers on Making Tax Digital; those who qualify for exemption must still meet the 31 October paper deadline.

The 31 January filing date explained

The 31 January deadline applies to online Self Assessment returns only. This date also serves as the Self Assessment payment deadline—if you owe tax, it must be paid by 31 January or interest begins accruing immediately. If you file after 31 January without a valid reason, HMRC automatically applies a £100 penalty.

Tax year 2025/26 specific dates

- Tax year ends: 5 April 2026 (not a filing deadline)

- Paper return deadline: 31 October 2026

- Online return deadline: 31 January 2027

- Payment deadline: 31 January 2027

- Late filing penalty starts: After 31 January 2027 (if filing late, late payment interest starts immediately)

What happens if you file late

Filing after 31 January triggers automatic penalties. £100 penalty applies if you file 1–3 months late. £300 penalty applies if you file 4–12 months late. Over 12 months late, HMRC may charge up to 5% of unpaid tax (or £300, whichever is greater). Daily interest also accrues on unpaid tax at the current HMRC rate (8.75% per annum for 2025/26).

Source: HMRC Self Assessment: Due dates and deadlines

[ Making Tax Digital compliance and software setup]

What Are Payments on Account?

Many self-employed individuals must make advance tax payments known as Payments on Account.

Key dates:

- First payment: 31 January

- Second payment: 31 July

- Each payment is normally 50% of the previous year’s tax bill

If your Self Assessment liability exceeds HMRC thresholds, you may be required to make these advance payments even if your next year’s income changes.

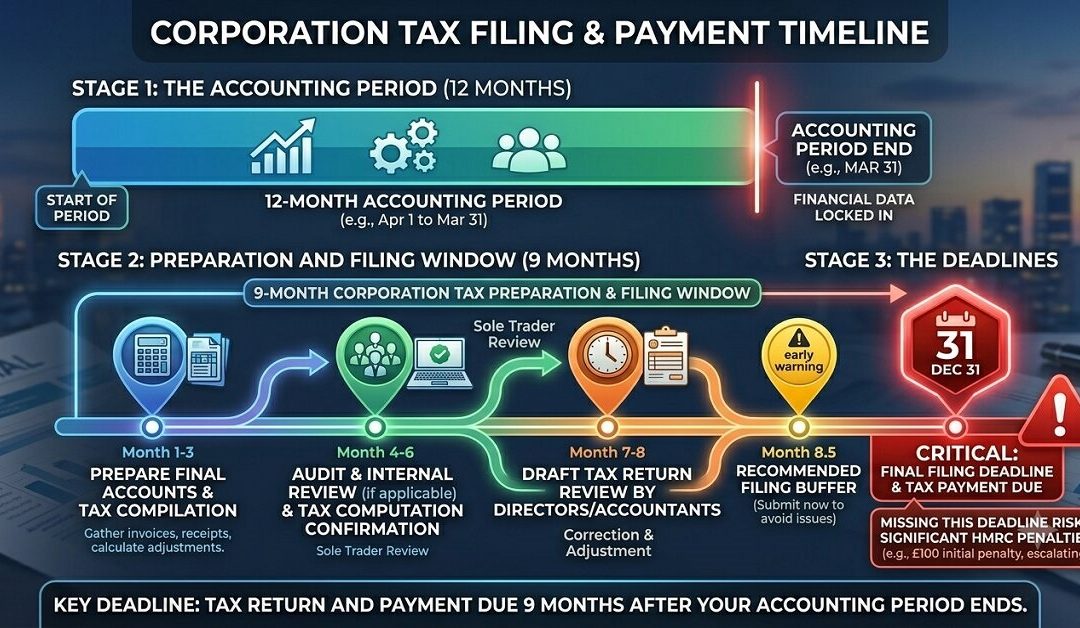

What Is the Corporation Tax Return Deadline for Limited Companies?

Limited companies must file their corporation tax return within nine months of their accounting period end. If your company’s accounting period ends 31 December 2025, your corporation tax return is due by 30 September 2026. If your period ends 31 March 2026, the return is due by 31 December 2026. Unlike Self Assessment, there is no automatic HMRC extension; you must request additional time in advance before the deadline passes.

The nine-month filing window explained

The nine-month deadline is firm and applies from the end of your company’s accounting period, not from the tax year end. This means different companies face different deadlines depending on when they choose to close their accounts. A company with a calendar year-end (31 December) has until 30 September to file; a company with a year-end of 30 April has until 31 January.

Accounting period end dates and filing deadlines

- Period ends 31 March: Return due 31 December

- Period ends 30 June: Return due 31 March

- Period ends 30 September: Return due 30 June

- Period ends 31 December: Return due 30 September

Tax year 2025/26 corporation tax dates

For accounting periods falling within the 2025/26 tax year (6 April 2025 to 5 April 2026), corporation tax returns are filed within nine months of your company’s specific period-end date. Many small companies align their year-end with 31 March or 31 December; verify your company’s year-end via Companies House records.

Streamlined returns and abbreviated formats

Small companies (turnover under £10.2 million for 2025/26) may file a streamlined corporation tax return. This reduces the volume of detailed information required but does not extend the nine-month deadline. If your company qualifies, speak to your accountant about using the abbreviated return format.

Important: Corporation Tax payment and Corporation Tax return deadlines are different.

- Corporation Tax payment is usually due 9 months and 1 day after the accounting period ends.

- The Company Tax Return (CT600) is generally due 12 months after the accounting period ends.

Always check HMRC requirements for your specific accounting period.

[ Corporation tax return filing for limited companies]

What HMRC Penalties Apply If You Miss the Tax Return Deadline?

HMRC penalties for late tax returns escalate significantly. A £100 fixed penalty applies automatically if you file your Self Assessment return 1–3 months after 31 January. This penalty applies even if you owe no additional tax. If you file 4–12 months late, the penalty rises to £300. Filing over 12 months late triggers penalties of up to 5% of unpaid tax (or £300, whichever is greater), plus daily interest accrual.

Penalty structure for late Self Assessment returns

- 1–3 months late: £100 fixed penalty (applies even if nil tax owed)

- 4–12 months late: £300 penalty

- Over 12 months late: Up to 5% of unpaid tax (or £300 minimum)

- Dishonest return: Up to 100% of unpaid tax (deliberate non-compliance)

Penalty structure for late corporation tax returns

Corporation tax returns follow similar escalation. £100 penalty for returns 1–3 months late. £300 for 4–12 months late. Up to 5% of unpaid tax over 12 months late. These penalties apply automatically; HMRC does not require a formal notice.

Interest charges on unpaid tax

Beyond filing penalties, unpaid tax accrues interest daily at the Bank of England base rate plus 2.5%. For 2025/26, this is 8.75% per annum. Interest starts accruing from the original payment deadline (31 January) and continues until paid. A £5,000 unpaid tax liability over six months costs approximately £219 in interest alone.

Cumulative cost of missing deadlines

A self-employed trader with £20,000 unpaid tax filed three months late faces: £100 late filing penalty + £1,312 interest over six months = £1,412 in addition to the tax itself. For a company filing six months late, penalties and interest can exceed £2,000 depending on the tax owed.

[IMAGE: Escalating HMRC penalty scale for late Self Assessment returns: £100 (1–3 months), £300 (4–12 months), 5% of unpaid tax (over 12 months), with daily interest accrual example]

⚠️ HMRC Warning: Penalties are applied automatically. You cannot appeal penalty cancellation without a valid reason (reasonable excuse). Simply claiming “I forgot” or “I was busy” will not succeed. See the section on extensions below for valid grounds to request penalty cancellation.

When Must You Register for Self Assessment?

If you become self-employed or start receiving untaxed income, you must register with HMRC by 5 October following the end of the tax year in which the income arose.

Failing to register on time can lead to penalties and may delay the issue of your Unique Taxpayer Reference (UTR).

Source: HMRC: Paying your Self Assessment bill and penalties

Can You Get a Tax Return Filing Extension or Reasonable Excuse?

Extensions are not automatic. You must request additional time by calling HMRC before the filing deadline passes. If you miss the deadline, you can only appeal on the grounds of reasonable excuse—circumstances beyond your control such as serious illness, bereavement, or a system failure preventing file access. Poor planning, accountant delays, or lost documents do not normally qualify as reasonable excuse.

How to request a formal filing extension from HMRC

Call the HMRC Self Assessment helpline before 31 January (for 2025/26) to request additional time. HMRC can grant a discretionary extension, typically 30–60 days. You must explain why you cannot meet the deadline. Acceptable reasons include: serious illness with medical evidence, unexpected bereavement, unexpected absence due to business emergencies, or proven technical failure of your accounting software.

What qualifies as a reasonable excuse

- Serious illness: You or a close family member seriously ill with medical proof required.

- Bereavement: Recent death of a close family member affecting your ability to file.

- System failure: Technical failure of HMRC systems (not your personal computer) preventing access to your account.

- Unexpected absence: Unexpected circumstances preventing you from accessing records (not holiday or planned absence).

- Not reasonable: Accountant delays, poor record-keeping, forgetfulness, or business pressure.

Timescales for extension requests

Request an extension before your deadline. Calling on 31 January to request more time may succeed, but waiting until February guarantees a rejection. If you cannot contact HMRC before the deadline due to circumstances beyond your control (e.g., system outage), document this in writing and include it in your reasonable excuse appeal.

Claiming reasonable excuse after the deadline

If you miss the deadline, write to HMRC within 30 days of receiving a penalty notice, explaining your reasonable excuse. Include supporting evidence (medical certificates, death certificates, software failure confirmations). HMRC will review and may cancel the penalty. This process takes 6–8 weeks; do not delay.

[ HMRC reasonable excuse appeal process]

Are There Different Deadlines for Making Tax Digital (MTD) Returns?

Making Tax Digital (MTD) is mandatory for self-employed and landlords with income over £10,000 annually since 6 April 2024. MTD returns must be filed online only; paper submissions are not accepted. The Self Assessment MTD deadline is 31 January (same as standard Self Assessment), but MTD requires quarterly reporting throughout the year in addition to the final annual submission. Failure to provide quarterly data or file the final return triggers separate HMRC penalties.

What is Making Tax Digital and who must use it

Making Tax Digital requires you to keep digital accounting records and submit quarterly summaries to HMRC automatically from your accounting software. The software must integrate with HMRC systems via a secure API. From 6 April 2024, all self-employed and landlords with income over £10,000 must use MTD. Smaller traders (under £10,000 income) can opt in voluntarily.

MTD submission deadlines for Self Assessment

Your final Self Assessment return is due 31 January 2027 for the 2025/26 tax year. Quarterly summaries must be submitted by: 5 July 2026 (Q1), 5 October 2026 (Q2), 5 January 2027 (Q3), and 31 January 2027 (final return). Each quarterly summary should be filed within a few days of your quarter-end; most accounting software does this automatically.

MTD deadlines for corporation tax and VAT

VAT returns under MTD are due within 7 days of the month (or quarter) end. Corporation tax returns under MTD follow the standard nine-month deadline from accounting period end but must be submitted online only. Partnership returns follow standard MTD Self Assessment rules.

Quarterly reporting requirements under MTD

- Quarterly updates mandatory (5 July, 5 October, 5 January, and 31 January for final).

- Software must be HMRC-approved and connected via secure API.

- Failure to provide quarterly data: £200 penalty per month (capped at £1,200 initially).

- Final return must be submitted online by 31 January; no paper returns accepted.

- Accounting records must be kept digitally from 6 April 2023 onwards.

How Long Must You Keep Tax Records?

HMRC generally requires taxpayers to retain records for:

- Self-employed individuals: at least 5 years after the 31 January submission deadline

- Limited companies: at least 6 years

- VAT-registered businesses: at least 6 years

Records may include invoices, receipts, bank statements, payroll information, and accounting software records.

Source: HMRC Making Tax Digital guidance

What Are Other Important Tax Deadlines You Shouldn’t Forget?

Beyond Self Assessment and corporation tax, several other critical deadlines apply. VAT returns are due within 7 days of the month (or quarter) end—much shorter than annual return deadlines. PAYE and National Insurance are due monthly by the 19th of the following month. Trust tax returns and partnership returns follow Self Assessment deadlines. Missing any of these triggers separate HMRC penalties and interest.

VAT return and payment deadlines

- Monthly VAT returns: Due within 7 days of the month end (e.g., 7 February for January return).

- Quarterly VAT returns: Due within 7 days of quarter-end (e.g., 7 May for Q1 ending 30 April).

- Payment deadline: Same as return deadline (7 days); pay via bank transfer or direct debit.

- Late penalties: 15% of unpaid VAT for first failure; 20% for second failure within 2 years; 30% for third within 2 years; up to 100% for deliberate non-payment.

PAYE and National Insurance payment dates

PAYE and National Insurance must be paid by the 19th of the following month (e.g., 19 May 2026 for April 2026 payroll). If you pay electronically, you have until the 22nd. Missing payroll deadlines triggers penalties of 3% of unpaid PAYE plus daily interest at 8.75% per annum. If you fail to submit a PAYE return within a month of the deadline, HMRC may issue a direction to recover the amount as a debt.

Trust and estate tax return deadlines

Trust tax returns (Form SA900) must be filed by 31 January following the tax year, same as Self Assessment. Estate tax returns after death must be filed within specified periods depending on the probate process. Trustees must also file quarterly partnership updates if the trust holds a partnership interest.

Partnership return deadlines

Partnership returns (Form SA800) must be filed by 31 January online (31 October paper) for the 2025/26 tax year. Individual partners then file personal Self Assessment returns including their share of partnership profits. If a partner files their individual return before the partnership return is submitted, HMRC may issue a penalty.

How Can You Prepare Now to Meet All Your Tax Return Deadlines?

The best way to avoid penalties is to prepare throughout the year rather than cramming in January. Create a tax deadline calendar marking all relevant dates for your business structure. Maintain accurate accounting records from day one using HMRC-compliant software. Engage an accountant by October to discuss tax planning and confirm filing arrangements. Implement quarterly management accounts to track profit and tax liability.

Create a tax deadline calendar for your business

- List all applicable deadlines: Self Assessment (31 January), VAT (7 days of month end), PAYE (19th of following month), corporation tax (nine months from period end).

- Mark internal deadlines three weeks earlier to allow for accountant review and corrections.

- Set calendar reminders on your phone and email on the 15th of each relevant month.

- Share the calendar with your accountant and bookkeeper to ensure alignment.

- Review the calendar quarterly to confirm no dates have changed or new obligations arisen.

Set up monthly accounting and record-keeping habits

Maintain records throughout the year. Do not wait until January to gather invoices and receipts. Implement cloud accounting software (Xero, FreeAgent, or QuickBooks Online) linked to your bank account and set up daily or weekly reconciliation. Keep all supporting documents—invoices, receipts, payslips, expense claims—in a dedicated folder (physical or digital) organised by month. This makes year-end compilation fast and reduces errors.

Organise supporting documents and evidence

- Invoice register: File all sales and purchase invoices chronologically.

- Bank statements: Reconcile monthly and keep copies with annotations.

- Receipts: Store digitally (photograph or scan) with the corresponding transaction noted.

- Payroll records: Keep payslips, NI records, pension contributions, and payroll reports.

- Contract and agreement records: Retain copies of service contracts and client agreements for six years.

Work with a qualified accountant early

Engage an accountant by October (before the rush) to discuss your tax position. A good accountant will flag deadlines, identify tax-saving opportunities, and confirm your filing method (online, paper, or Making Tax Digital). They will also prepare a timescale for completion: typically November–December for accounts review, January for final return submission.

💡 Pro Tip: Set an internal deadline 21 days before the HMRC deadline. If you file by 10 January for 31 January submission, you give yourself time to correct errors without rushing. This buffer prevents last-minute panic and ensures quality.

People Also Ask

Can HMRC reject a second tax return if I file twice by mistake?

If you file your Self Assessment return twice, HMRC will automatically process both. The second return is treated as an amendment under standard rules. You cannot delete a submitted return; you can only amend it via your HMRC online account within 12 months of the 31 January deadline. Contact HMRC directly if you have filed duplicates; they will guide you through the amendment process.

How do I amend a submitted tax return?

Log into your HMRC online account and select “Amend your tax return.” You have 12 months from 31 January after filing to amend. Changes to income, expenses, or personal details can be made within this window. HMRC will recalculate your tax and issue a revised statement. Amendments filed after 12 months cannot be made online; contact HMRC directly or request a correction via your accountant.

What happens if I forget income on my tax return?

If you discover forgotten income after filing, amend your return immediately via your HMRC online account (within 12 months of 31 January). The sooner you report the error, the lower the interest accrual. HMRC may impose an enquiry penalty if the amount is substantial, but reporting errors voluntarily often results in penalty cancellation under HMRC’s “careless” rather than “deliberate” category, reducing the penalty from 100% to 30% of unpaid tax.

Can married couples submit a joint tax return in the UK?

No. Each individual must file their own Self Assessment return with their own UTR number. There is no joint return option. However, you can claim Marriage Allowance if one spouse has unused allowances, transferring unused personal allowance to the other. Both individuals must have separate HMRC accounts and file individual returns.

Frequently Asked Questions

When is the deadline for filing a Self Assessment tax return online in the UK?

The deadline for online Self Assessment returns is 31 January following the tax year end. For 2025/26, this is 31 January 2027. Paper returns must be filed by 31 October 2026.

What happens if I miss the tax return deadline?

HMRC automatically applies a £100 penalty if you file 1–3 months late. Filing 4–12 months late triggers a £300 penalty. Over 12 months late, you face up to 5% of unpaid tax. Interest also accrues daily on any unpaid tax.

How long do limited companies have to file a corporation tax return?

Limited companies must file their corporation tax return within nine months of their accounting period end. If your period ends 31 December 2025, you must file by 30 September 2026. Extensions must be requested in advance.

Can I get an extension if I can’t file my tax return on time?

Extensions are not automatic. Call HMRC before your deadline to request extra time. After the deadline, you can only appeal based on reasonable excuse (serious illness, bereavement, or system failure). Accountant delays do not normally qualify.

Is Making Tax Digital mandatory for my self-employed business?

Yes, Making Tax Digital is mandatory if you are self-employed or a landlord with income over £10,000 per year (since 6 April 2024). You must keep digital records and submit returns online only. Quarterly summaries are also required.

What are the VAT return deadlines and how do they differ from Self Assessment?

VAT returns are due within 7 calendar days of your return period end (monthly or quarterly). Self Assessment returns are due 31 January. These are completely separate deadlines. Missing VAT deadlines triggers separate penalties starting at 15% of unpaid VAT.

Do I Need to File a Tax Return If I Made No Profit?

Possibly. HMRC may still require a return if you are registered for Self Assessment, operated as a sole trader during the year, received rental income, or received a notice to file. Even where profits are low or nil, filing obligations can still apply.

Before You Submit — Checklist

- ☑ Employment income included (P45 or P60)

- ☑ Self-employment income included (invoices and receipts)

- ☑ Rental income included (rent received less expenses)

- ☑ Dividend income included (dividend vouchers or company records)

- ☑ Bank interest included (bank statement confirmation)

- ☑ UTR confirmed (on HMRC letters or online account)

- ☑ Return reviewed by accountant or qualified advisor

- ☑ All supporting documents retained for six years

- ☑ Personal information (address, contact) up to date

- ☑ Payment plan or funds arranged if tax due

HMRC Digital Account Checklist”

Before Filing Online

- ✔ Government Gateway account active

- ✔ UTR number available

- ✔ National Insurance number confirmed

- ✔ Bank interest records collected

- ✔ Dividend records gathered

- ✔ Pension contribution details available

- ✔ Business expenses reviewed

- ✔ Supporting documents retained

Useful HMRC Contacts

- Self Assessment Helpline

- Corporation Tax Helpline

- VAT Helpline

- Online Services Helpdesk

Check the latest contact information directly through HMRC before calling, as telephone services and opening hours may change.

Sources and References

Official Sources Used

- HMRC Self Assessment Guidance

- HMRC Corporation Tax Guidance

- HMRC Making Tax Digital Guidance

- HMRC Penalties and Appeals Guidance

- HMRC VAT Returns Guidance

Expert Insights: How We Help You Stay Compliant

Our ICAEW-qualified team at Eternity Accountants has worked with hundreds of small business owners and self-employed professionals navigating UK tax deadlines. The most common mistake we see is underestimating the impact of missing a deadline. A single £100 late filing penalty might seem minor, but combined with interest charges, appeals, and administrative stress, it costs far more than proactive planning.

The second mistake is confusing paper return deadlines (31 October) with online deadlines (31 January). Many traders believe they must file by October and either file unnecessarily early or file late and incur penalties. Online filing is mandatory under Making Tax Digital for almost all self-employed and landlords, giving you an extra three months.

Our approach is to build a tax calendar with each client at the start of the financial year, marking all deadlines relevant to their business structure. We implement quarterly check-ins to review profit, tax liability, and potential tax-saving opportunities. This proactive approach eliminates last-minute panic and unexpected penalties. For clients with multiple income sources (employment plus self-employment, or partnership income), we confirm upfront whether separate Self Assessment returns or supplementary pages apply.

We also help clients understand reasonable excuse claims. HMRC is more lenient with genuine circumstances (serious illness, bereavement) than with poor planning or forgetfulness. If you do miss a deadline, contact us immediately; we can help you prepare a reasonable excuse appeal with supporting evidence and maximise the chances of penalty cancellation.

Real-World Example: From Stress to Compliance

Client scenario: A freelance marketing consultant with £45,000 annual income missed the 31 January Self Assessment deadline by 12 weeks. Despite having no additional tax to pay beyond what she’d already submitted through PAYE, she received HMRC penalties totalling £450 (£300 late filing + estimated late payment interest of £150 over six months).

Before: No tax deadline system in place. Records scattered across email. Invoices filed in desk drawers. No contact with an accountant until February when filing became urgent. She believed the paper deadline applied to everyone and thought she had time.

After: She implemented cloud accounting software (FreeAgent) with automated client invoice tracking and reconciliation. Set calendar reminders on her phone and email: October (first quarterly check-in), December (final review), January (submission deadline). Scheduled quarterly calls with a bookkeeper to review tax position and identify tax-saving opportunities.

Outcome: The following year, her return was filed on 15 January without penalties. Tax liability was predicted accurately by December, allowing time for payment planning. Stress reduced by 80%. She has since received three years’ on-time filing status with HMRC, building a strong compliance record.

Common Mistakes to Avoid

- Confusing paper deadline (31 October) with online deadline (31 January): Many self-employed incorrectly believe they must file by 31 October. Only paper returns have this earlier deadline. Online returns get three extra months to 31 January. HMRC penalty if you file between 1–3 months late: £100.

- Assuming corporation tax deadline extensions are automatic: Unlike some jurisdictions, HMRC does not automatically extend the nine-month corporation tax deadline. Extensions must be requested in advance before the deadline passes. HMRC penalty for 1–3 months late: £100 starting penalty, escalating to £300 for 4–12 months late.

- Blaming your accountant for late filing and hoping HMRC will accept “reasonable excuse”: HMRC guidelines state that relying on your accountant is your responsibility. Accountant delays do not normally qualify as reasonable excuse. HMRC penalty: £100–£300 plus interest. Reasonable excuse appeal rejected if accountant delay is the sole reason.

- Mixing up VAT deadlines (7 days) with Self Assessment deadlines (31 January): VAT returns are due within 7 calendar days of the month (or quarter) end. Self Assessment is due 31 January. These are completely separate deadlines. VAT late penalties: 15% of unpaid VAT (first failure), 20% (second within 2 years), 30% (third within 2 years), up to 100% for deliberate defaults.

- Not realising Making Tax Digital requires quarterly reporting, not just year-end filing: MTD is not simply an annual submission via software. Eligible taxpayers must keep digital records and submit quarterly summaries to HMRC in addition to the final annual return. MTD non-compliance penalty: £200 per month (capped at £1,200 per year initially).

How Eternity Accountants Can Help You Stay on Track

We manage tax deadlines so you can focus on your business. Our services include:

- Self Assessment filing: End-to-end preparation, review, and online submission by deadline. We handle all supplementary pages, capital gains, and dividend reconciliation.

- Corporation tax returns: Nine-month deadline tracking from your accounting period end. We prepare returns, negotiate with HMRC enquiries, and claim research and development relief where applicable.

- Making Tax Digital compliance: Software setup, integration testing, and quarterly report submission. We ensure your accounting software is HMRC-approved and connected securely.

- VAT and payroll deadlines: Automated tracking, return preparation, and payment arrangement coordination.

- Penalty appeals and reasonable excuse claims: We prepare detailed appeals with supporting evidence and negotiate with HMRC on your behalf.

- Year-round tax planning: Quarterly management accounts, tax liability forecasting, and identification of reliefs and deductions you may have missed.

Contact Eternity Accountants today to discuss your tax deadline obligations and how we can support your compliance.

Conclusion: Take Control of Your Tax Deadlines Today

Understanding when tax returns are due is fundamental to avoiding costly HMRC penalties and interest charges. Self-employed and landlords must file by 31 January online (or 31 October for paper). Limited companies have nine months from accounting period end. VAT, PAYE, and Making Tax Digital each have their own separate deadlines. Missing deadlines triggers automatic penalties starting at £100, plus interest accruing daily on unpaid tax.

The best approach is proactive planning: create a tax calendar marking all deadlines, maintain accurate records throughout the year, implement HMRC-compliant accounting software, and engage an accountant early. Quarterly check-ins help you stay on track and identify tax-saving opportunities before year-end.

Do not wait until January to think about tax deadlines. Start now, set your internal deadlines three weeks ahead of HMRC deadlines, and build a sustainable compliance routine. Eternity Accountants’ ICAEW-qualified team is here to guide you through every deadline, every year. Contact us today to set up your tax calendar and eliminate deadline stress for good.

Reviewed By

This article has been reviewed by the ICAEW-qualified accounting team at Eternity Accountants. Our chartered accountants specialise in Self Assessment compliance, HMRC investigations, and tax planning for UK small businesses and sole traders. We have guided hundreds of self-employed professionals and company directors through deadline compliance, penalty appeals, and strategic tax planning. Eternity Accountants is ICAEW-regulated and AAT-accredited.

Last reviewed: June 2026